One of the most irksome tasks of owning an eCommerce business is keeping track of inventory—not just the number of units, but their costs. The bigger your business, the harder this becomes. Of course there are eCommerce fulfillment software and inventory management systems that can do this for you, but every business owner should know the basics of inventory accounting methods. Without them, you’re flying blind.

Knowing how to calculate the value of your merchandise inventory is a big deal for lots of reasons. Most importantly, it goes into the formula to calculate the cost of goods sold (COGS) which determines whether or not your business is making a profit. Oh and, btw, it’s also a number you need to know at tax time, because it goes into calculating your net income and, ultimately, your taxable income.

So how do you calculate inventory costs? There are several methods, and Weighted Average Cost is one of those methods. Stick with us and you’ll find out what WAC is, what other options you have, and which one is right for your business.

What You Need to Know about Inventory Accounting Methods

The four inventory valuation methods used in accounting are:

- FIFO (first in, first out)

- LIFO (last in, last out)

- Weighted Average Cost

- Specific Identification

Each method is a different way of assigning costs to each physical unit of merchandise that flows through your business each year. These costs go into calculating the cost of goods sold, as well as the value of your ending inventory (the merchandise inventory you have left at the end of the year).

As an eCommerce business owner, If you have an accountant, one of the first decisions they’ll ask is which inventory cost flow method you want to use. Because this decision affects profitability as well as taxable income, you should understand the pros and cons of each method. Once you make a decision, you have to stick with it for the sake of consistency (and because the IRS says so).

For most eCommerce businesses, inventory costs include the purchase price, freight, labor to get it on the shelves, and storage. For eCommerce businesses that manufacture their own goods, inventory costs include the cost of raw materials used, direct labor, packaging, and indirect costs such as overhead and administration. Because these costs are not static (in most cases they’re rising) inventory valuation methods (also called cost flow assumptions) were standardized to make inventory valuation easier and more consistent year over year.

Your accountant can help you decide which method is best, based on factors that include the size of your company, the types of inventory you carry, supply chain dependencies and, not incidentally, the economic conditions of the day. It’s not impossible to switch methods down the road, but because you have to apply for permission with the IRS to do so, it’s best not to switch unless absolutely necessary—and sometimes you can’t switch back.

Inventory Valuation Methods

First In, First Out (FIFO)

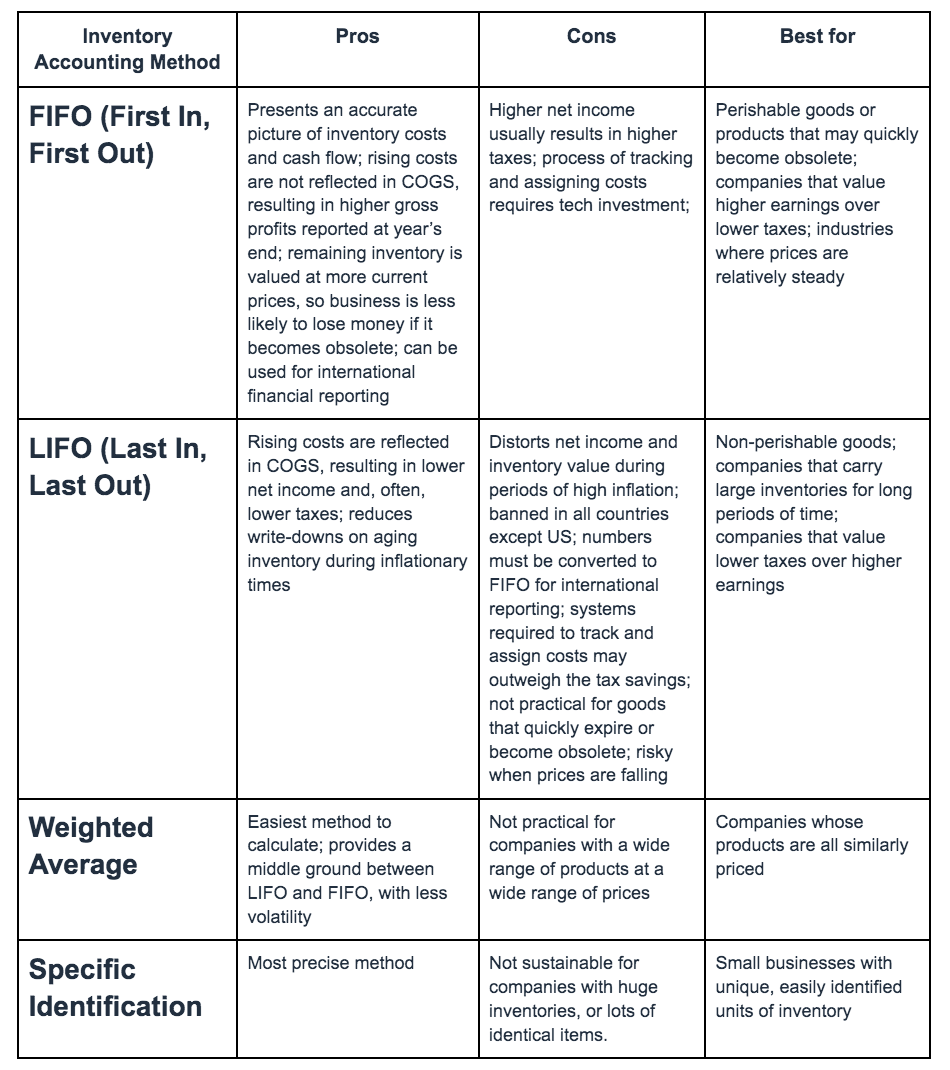

The FIFO inventory method assumes that your inventory is being sold in the order it was purchased. When calculating cost of goods sold, the cost of the oldest item in the warehouse is attributed to the first item sold in a given year, regardless of which item is grabbed off the shelf. The cost of the second oldest item in the warehouse is assigned to the cost of the second item sold, and so on. Because the cost of goods tends to rise over time, the FIFO method usually results in lower cost of goods sold at year’s end, which translates to higher profits. In addition, your greatest asset, the remaining or “ending inventory,” is valued at its actual (usually higher) cost. Most companies use the FIFO method, because it paints a more accurate picture of income and actual costs, and matches the ideal physical flow of products.

Last In, Last Out (LIFO)

The LIFO inventory method assumes that the newest inventory is sold first. When calculating cost of goods sold, the cost of the most recently purchased item is the cost attributed to the first item sold each year. Because the cost of purchasing goods tends to rise over time, COGS, as reported under LIFO, is usually higher than what the company actually paid. This results in lower profits, lower net income and, often, lower taxes at year’s end. In addition, because the newer inventory presumably was sold first, the remaining or ending inventory may be years old or obsolete, so its calculated value will be lower than with other accounting methods. Companies that hold inventory for long periods of time tend to benefit from the LIFO method. Because the LIFO method distorts net income and inventory value during periods of high inflation, international accounting standards have moved away from using it. While LIFO is still accepted in the U.S., it has been banned in all countries that follow international accounting guidelines. Some companies use LIFO for inventory management and FIFO for tax reporting. Only a few large U.S. companies still use LIFO for tax reporting.

Weighted Average Cost

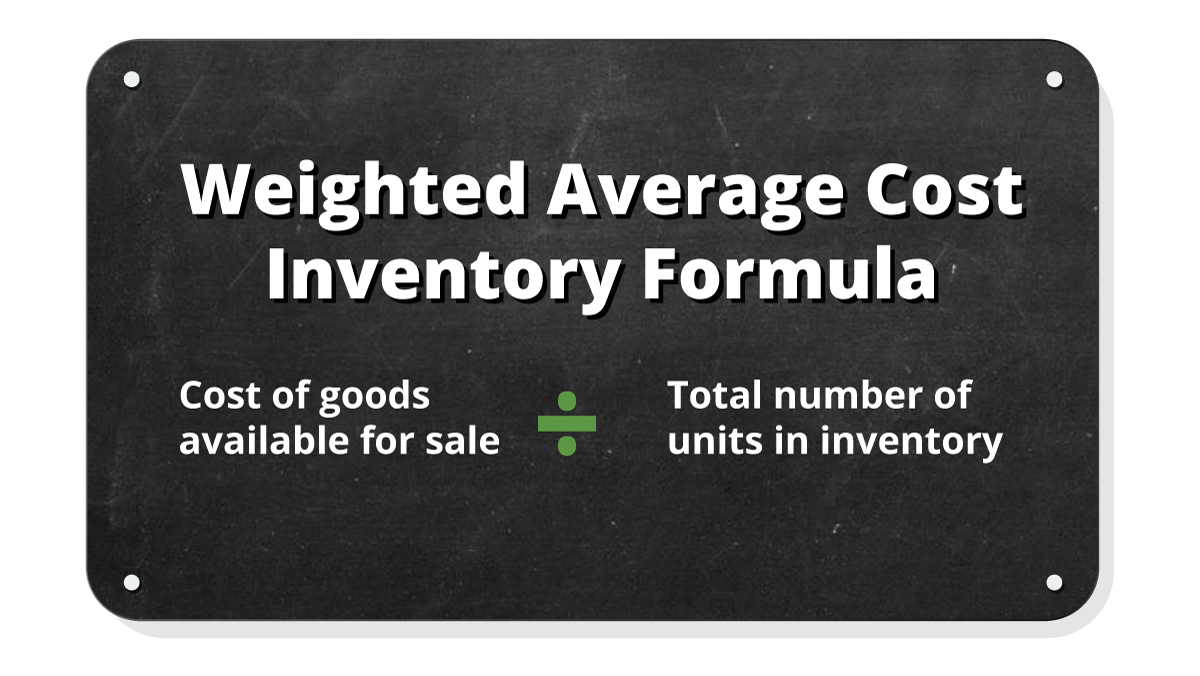

Under the Weighted Average inventory method, all costs are averaged. The cost of all purchased goods (including any left over from the prior accounting period) is divided by the number of units to arrive at an average cost per unit. COGS can then be calculated by multiplying the number of units sold by the average cost per unit. Likewise, ending inventory value is calculated by multiplying the number of units left by the average cost per unit. The weighted average cost method is the easiest inventory accounting method to manage, but not very practical if the cost of your products varies widely.

Specific Identification

This method assigns an exact cost to each unit of merchandise. It is the most precise method if you have the ability to track each individual unit purchased or sold. Understandably, it gets more difficult to manage as your business grows, or if you sell more than one of the same SKU.

Pros and Cons of Inventory Accounting Methods

One Important Note: Cost flow assumptions are just that—assumptions. Actual costs are recorded when inventory is purchased or (for manufacturers) when items move from production into finished goods. As those costs rise or fall, accountants may or may not assign a different cost to that particular unit of inventory, depending on the method chosen.

Another Important Note: Cost flow assumptions are only used in accounting. They have nothing to do with the way goods are physically rotated on and off the shelves. In other words, you can rotate stock using first in, first out, but use a completely different method to calculate COGS and inventory costs. That’s 100% okay.

Periodic vs. Perpetual Inventory Accounting

In addition to the choice of inventory cost methods, you have a choice in how closely you want to track inventory. Periodic inventory is the practice of physically counting items in stock at regular intervals, usually at least once a year. Some inventory may be counted more often to maintain inventory levels on fast-moving items, but large businesses may have to wait until the end of the year to know where they stand.

Perpetual inventory systems use software to update inventory counts (and costs) the second an item is sold. Inventory management systems integrate with warehouse management systems or eCommerce fulfillment software platforms to provide real-time access to these figures for accounting and finance teams, as well as inventory managers.

Using a periodic inventory system with the weighted average cost flow assumption, the average cost per unit is calculated after the year is over and all purchases have been made. The average cost per unit is then applied to all units sold that year, as well as to the leftover units in inventory at the end of the year.

Using a perpetual inventory system, your eCommerce fulfillment software is constantly updating the average cost per unit each time an item is sold. The cost of the item sold (COGS) is recorded as the average cost at the time of the sale. The system then automatically calculates a new average cost per unit for the remaining items in inventory. Order fulfillment software integrates with inventory management systems and accounting systems, so these figures are available 24/7 to anyone who is given access.

Weigh Your Options

The weighted average cost method is one of several inventory accounting methods, and one of the simplest. It may or may not be the right choice for your eCommerce business. Since inventory costs are usually an eCommerce company’s greatest asset, it’s worth your while to learn the nuances in how these costs are calculated using different methods.

If your order fulfillment software or 3PL provider doesn’t have the technology to make these calculations easier for you, it might be time to make a switch. A tech-forward 3PL like ShipMonk can simplify all of this with a user-friendly software platform that puts inventory numbers at your fingertips. Contact ShipMonk for a quote, or request an eCommerce fulfillment software demo that will blow your socks off!